The B Word You Need to Hear

40sOpens with a playful, attention-grabbing hook about 'budget' and challenges procrastination, relatable to many.

▶ Play Clip[00:00] Okay, you guys, this is the video that you have been waiting for. It's time to talk about the B word. Not that B word, get your head out of the gutter. Budget.

[00:14] Today, consider me the Oprah of budgets. You get a budget. You get a budget. You get a budget. No, today. Right now.

[00:27] We've all said it before. I'll start tomorrow. I'll start next week. I'll start next month. You know when that is? Never. Your procrastination ends now.

[00:40] Okay, in all seriousness, this is our heart to heart person to person get your ish together chat in about 30 seconds I want

[00:54] you to press pause I want you to go get your favorite beverage coffee soda water tea whatever you need to get the wheels going you know what I'm talking about go get a pad of paper

[01:10] go get a pen or pencil, and get a calculator. The time is now. Who the heck am I? My name is Kate, and I am not a finance expert by any means. I am just like you. We are the same. I am a single

[01:28] parent with a fabulous five-year-old child. In the last few years, I've been able to save enough money to write out a fact check to pay off my car for $20,000 and I've also been able to save up a

[01:42] six-month emergency fund all while being a single parent with many jobs. If you're curious about what I do for work, I'm an administrative assistant. I'm also a choreographer. I will link a video here of

[01:55] all the jobs that I participate in so you know roughly what I do with my time. But beyond work, I'm a mother, I'm a sister, I'm a daughter, and I want to have the best life I possibly can for me and my son, my family, my friends.

[02:12] I want to really maximize the budget that I have. So today I'm going to teach you how to create a budget. If you've never created a budget before, congrats on starting now. The first budget I ever did was in the month of July, so I feel like this is appropriate because you can start yours for the month of July.

[02:31] right now. If you've seen my how to save money video you'll know that my budget items are actually called some really different names than I would normally refer to but in the interest of any new viewer watching I'm not going to suggest

[02:45] you to that today but I will leave this video here of how I actually name my budget to make it more fun and exciting when you're budgeting. Here we go the first thing you should know is I want budgeting to be as simple as possible. I

[03:01] I know I've watched a million budgeting videos, and I think that most of my knowledge that I actually utilize comes from Jordan Page from Fun Cheaper Free. I think she has great tips mixed with some Dave Ramsey.

[03:17] I think he's got some outstanding information. And then also all the other budgeting YouTubers that have paved the way. This is why you're watching me right now is because others have done it. and they set a great example on how to share their information.

[03:31] And that's what I'm hoping for you, that I can share with how I budget so that we can get you in the best financial position possible so you can sleep at night, so you can not be worried about bills constantly.

[03:43] There's nothing worse. You have mouths to feed, including your own, and no matter what your family situation is, I think this budgeting technique will help. Okay, did you pause the video and get your beverage?

[03:55] Because now is the time. If you haven't paused, do it now. Pause. Get your drink. Get your pad of paper, pen, pencil, calculator. That's all you need to get this started. Okay?

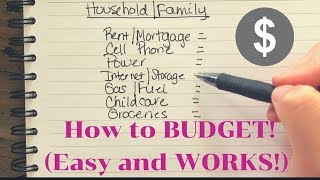

[04:07] Press pause. I'm waiting. Okay, I believe you. You're back? Let's do this. The first thing I do is focus on household slash family.

[04:22] Now, these are the things you need every single month that are kind of, I don't want to say completely non-negotiable, but pretty non-negotiable.

[04:36] Let's get started so you can see what I'm talking about. The first thing you need is rent or mortgage. The second thing you need, for me, is cell phone.

[04:54] Next, power for your home. See, these are things, I mean, for me, I don't have a landline, I have just a cell phone,

[05:09] but I think a lot of people just have cell phones now, but whatever that is for phone, power. I have internet. And for me, because of YouTube, and just I have a lot of videos and

[05:24] pictures and stuff, I pay for extra storage. So that's one for me, this might not be for you. It's only like an extra $5 a month, but everything adds up. Next is gas for my car, fuel.

[05:37] Now, if you had a car loan here, I would put car, and then I would put car insurance. I pay my car insurance in a lump sum, so I don't have that as a monthly.

[05:52] It'd probably be around, you know, $45 a month if I put it in, but I don't have it because I pay it in a lump sum. Child care. For me, child care is a must.

[06:06] It's a non-negotiable. I have work and he must go to childcare part of the time. Childcare and groceries. So let talk about this If you were to lose your job tomorrow you still need a roof over your head Most of us would still need a phone I mean I think that pretty common but

[06:29] whatever you got to do. Power, you need to have electricity in your house. Internet might not be 100% necessary, but for me and with my YouTube job, it is.

[06:43] gas fuel for your car to get wherever you need to go, childcare if you work outside the home, you'll need that, and groceries, you gotta eat, people.

[06:56] You gotta eat. If I had debt, I would absolutely put that in this category. Because say you've got like a student loan, you've got a $25 credit card, another small $25, another $50, another $100.

[07:10] guys that could be 300 more dollars in your regular budget to put toward something more productive than paying interest on stuff you bought months ago

[07:22] I'm gonna fill this out and get around some numbers these are not my exact but For this today, I'm going to say $985, power 95, internet storage 75, gas fuel 75, child care.

[07:47] And for my groceries, just so you know, I usually do around $300 to $350. But for today, I know people aren't really down that far yet with their groceries, or some are more or even further down.

[07:59] But I'm going to say $400. I'd say like $100 a week is, you know, probably more average than what I actually spend, which is a little less than that. And then I don't have any debt.

[08:11] But let's say you have, I'm going to say $200 for this example. This comes out to $2,175.

[08:24] And like I said, I don't have debt, but in this example, $2,175, you know, thinking about like $2,000 for normal cost of living.

[08:38] If you didn't have that debt, you'd be at $1,975. Doesn't this look better than this? moving on the next category I have is giving now my first July budget I had this is what I had

[08:57] I had five dollars that I had to spare that first month but guess what I gave it away my five dollars I donated and that's all I had to start to start but hopefully

[09:10] you will have more eventually. But I swear if you start with a giving heart, even if it's $5 to start, it is training you to give and not feel so attached to money because I have been so attached to money

[09:24] my whole life. And this was the most freeing thing I ever did was starting to give some of it away. For our budget stake, I'm going to say you budget $25. And this could be for charities,

[09:37] if someone has a run, that you're sponsoring, anything like that. I'm just going to start with this for now because you might not have any extra money, but I swear if you put a little bit, for every reason I just said,

[09:49] it will help you and it will help others. And it will start priming your heart and your budget for a surplus. I hope that makes sense. Next is lifestyle.

[10:03] Lifestyle. these are all for me really optional I have a Kate budget I have a Caden budget

[10:15] I have a gym budget for Kate Caden has gymnastics you guys know I have a house cleaner and I know this was controversial for a few of you

[10:31] this one, this one, and massages, if I had any debt, and actually that one, this would all go away. If I had any debt,

[10:47] while I was paying off the debt, these would be gone. But right now, I have the means to do it, and I'm still saving money. There are things I choose to do with my money, because I can at this point. But back when I had debt, nope, no way. Now, okay, this is going to vary from person

[11:06] to person. For me in real life, it's probably about $100. That's what I do. But I'm going to say for someone that is just starting out, let's start with 50. And this, if you have any debt,

[11:20] like we talked about above, none. Okay, I wouldn't put any of that. I don't know if this is realistic, but depends how tight your budget is, you guys. I don't know what you've got going on. You have to be realistic. So $50, what this would be is if you need, you know, anything you want. This is really

[11:40] like whatever you want. I, if I was in debt, I probably wouldn't go get my nails done, but say you can fit it in there. Say Kaden needs a new pair of shoes. That was where I grabbed this from, that kind of thing. These are like my, oh, and then out to eat. Out to eat, again, completely

[11:59] optional, but for me right now, my real number is about $100 a month. In the summer, this goes a little bit high, but I'm going to say this for now in the context of this budgeting

[12:11] video. These are the things, you guys, that it's not necessary. So if you, like I said, when the catastrophic happens, you have to make sure these are covered, okay? That's the main thing.

[12:25] Giving, of course, is optional, but again, I just think changes you in a way that you will find beneficial, even if it's $5. Lifestyle, like I said, these would not be in it and they weren't until later.

[12:40] Out to eat, you don't have to have 100. You can have much less than that You can have a no out to eat budget whatever worked for you And now what is most important here

[12:52] I'm going to put it in big letters. Savings. For me, savings, I lump my retirement with my savings. And if you know, what I call this really is future, Kate, because I'm thinking about the future.

[13:11] So, let's imagine your income is $3,000. This might sound like a lot for some of you. This might sound not like a lot for some of you.

[13:24] $3,000, if you make $3,000 a month, that's saying you make about like $36,000. But I'm saying, let's pretend your take-home is $3,000, okay?

[13:40] take home $3,000. If I'm here, this was my household. This was my giving. These are my lifestyle. We're to $2,400. That means we have $600 left. Now, with $600, you could do a couple

[13:57] things. I would absolutely put it in your 401k or 403b as I have. Eventually, I would do a Roth IRA.

[14:12] If you have a 403b at work or a 401k and they match, I would totally do it to the match. if you don't have this probably not offered through work I do this on the

[14:25] side I use fidelity and the maximum you can contribute is $6,000 a year now you guys might not be worrying worry about this right now because we are beginning

[14:38] budgeting but just know in the future hopefully you can head toward this do you have some savings for retirement so with $600 you could either put a hundred in here, put $100 in here, and then put $400 in savings. Whatever is most comfortable for you,

[14:57] but you want to be putting some money in savings, you guys. You want to start stockpiling up that money. If you don't have an emergency fund, you need one. Most people say to start with $1,000

[15:13] and go from there, you need an emergency fund. Like I said, I've saved up for six months and that took a while, but like for this person, two, this, I'm just going to roughly say $2,000. Okay.

[15:31] Roughly 2000. And if you didn't have any debt, it really is. That would be, if you're going to do three to six months, you're going to have at least $6,000. Okay, you'd be aiming to save at least

[15:47] $6,000 if you want three months. If you want to have your six months, you'd be looking to save up $12,000 with a $2,000 per month basic needs. When I'm factoring in what I need for my emergency

[16:07] fund, I'm only dealing with this because if I lost my job or something catastrophic happens, all this would temporarily go away until conditions improved. So while we're at it, in case I haven't mentioned this, if any of these things can be lowered, if you can live

[16:22] in a smaller, more affordable home, that could be an option. Cell phone, household AT&T, that is totally what I did to get that down. This used to be up around like 115 or so. Power, you know,

[16:37] there's many ways you can work on that. Internet, you can try to get it down. Gas, you can always use less gas, but you got to get where you need to go. Childcare, find the best place that you

[16:49] can possibly afford. Groceries, that can always be worked on a little bit. Debt, kill that debt as fast as possible. So, okay, back to down here. If we were saving and I had debt,

[17:07] this debt, 100% to the debt, I would just get rid of it. You guys, when you don't have those debts anymore, your credit card debt, your student loans, you are going to feel so free and proud of

[17:22] yourself that you don't have that hanging over your head anymore. It's like a dark cloud that needs to go away. I think having four categories is way more manageable than having a million

[17:35] categories. I hope when you look at that, you're kind of like, all right, that's kind of simplified and it's just basic math. I don't like getting into cat food fund and haircut fund and blah,

[17:51] are too confusing for me. So I lump it together. So again, the main categories, household and family, giving, lifestyle and savings. It's also important to note, you need to know how

[18:06] much you make. I get it. A lot of people don't want to look at their numbers. It's scary. It's unsettling. It's anxiety inducing. But if you really want to take care of this problem,

[18:20] You've got to face it head on, you guys. Right now, I hope you're doing it right now. I hope you're writing out what your numbers are so that you can see, do I have any money left? What if you don't?

[18:32] What if it's in the negative? What if I had just done that and the bills had come up to $3,200 alone? What are you going to do? You know what you've got to do. You've got to comb through this budget.

[18:45] What can I take out? What's not necessary? Now, this, I think when you look at this, I bet you guys have a lot more line items than me at first. I think I used to have a lot more line items when I started this out.

[18:57] But as I practiced frugal living and minimalism techniques I just tried to be a lot happier with a lot less And it has made my life so much more simple and pleasurable and not so stressful Additional thoughts

[19:15] I get paid the 15th and the 30th of every month for my normal job. And when I'm budgeting, I was specifically asked to do a pen and paper budget,

[19:27] and that's why I did it this way for you guys, because I think everyone can easily do this. I say easily, but I don't mean easily. This is hard when you're trying to narrow things down, when you're trying to decide what's really important, when you're deciding that when you

[19:43] go into Target for laundry detergent, you come out a hundred dollars later with crap you don't need, that that's not going to get you where you need to go. And I have been there, my friends, I have been there. A lot of people get paid twice a month when I'm doing my budget. I just, that's the

[20:01] amount that I have. So say we were doing the $3,000 budget, say the first check $1,500, the second $1,500, I put that all in. If you have a more irregular income, you have to kind of average that out.

[20:15] And then when you're averaging, go low. Don't overestimate what you think. Go low. The other thing is, when I do this, like I said, I was doing this pen and paper upon request, which I think,

[20:28] I hope it's helpful for you guys. I input this all into EveryDollar, which is like a pen and paper, but a program. And EveryDollar is completely free. I use the free version.

[20:40] I'm not even going to encourage you to use that right now. Do this to start. This does the same thing. That just, it gives you like the percentages on the side of how much you're spending in each category. I just visually like to look at that.

[20:53] But that's not the most important thing. This is the most important thing. the bread and butter, the guts of it. You need to know how much you are getting and how much is going out. If you're in the position when you do this and you are hundreds of dollars over your

[21:09] budget, back to what I was saying, you need to comb through. You need to see what you can decrease slightly or you need to get another job. You need to increase the income or if you have a

[21:22] spouse that has extra time. Maybe they need to add the income. In the end, you've got to know you can do this. And if you're in debt and this is stressing you out and it's causing you anxiety,

[21:36] you can dig yourself out. I want you to know that. I don't want it just be words. I want you to put it all down, write it all out. See if there's anything you can either get rid of completely.

[21:50] there's some stuff you just like like cable cut there's many there's many things that you probably could cut that that you don't even think about but when you write it all out you're like oh crap costing me a thousand dollars a year that I didn't even realize or get a part-time job on top of the

[22:09] job and I know you're like oh I don't want to do that but sometimes you gotta dig deep temporarily to get to the other side. It's going to be okay. You can do this. This is probably a very lengthy

[22:24] video, but I'm not going to stop until it goes into your brain that this is doable right now for July. Like, let's get it together this month so that three months from now, say you get this

[22:39] budget ready for July. You do it July, August, September. Those three months are going to be your mess around month. You're not even going to know what's happening. Know it. Know the net. The

[22:51] first three months are the most eye-opening, the most freaky, the wildest three months of why am I even spending on that? It's eye-opening. Give yourself three months of wiggle room

[23:08] to get those wiggles out of financial astonishment. So after those initial three months, so we've got July, August, September, then fall's coming, and October, November, December,

[23:23] you're going to have your ish in order so that this Christmas could be possibly the first Christmas that you don't feel sick leading into it, buying gifts for others.

[23:35] The first Christmas you could actually pay is cash. Maybe it won't be this Christmas. That's only six months, but guess what? By Christmas, you're going to be six months deep in this,

[23:47] and I guarantee you'll pay off something. You'll be further along. But if you keep throwing your bills in the drawer, and you keep getting the mail and not looking at it, and you don't look at what your bank statement says,

[24:00] and you don't know what your pay stubs are, You're not going to be any further along at Christmas, and then the new year is going to come, and you're going to say, ooh, 2020 is coming. This is going to be my year.

[24:12] Maybe I should set a budget. No! Do it today. Then by the new year, you're six months along. Half a year of saving or paying off debt. It's going to be beautiful.

[24:26] Can you feel it? You get a budget. You get a budget. Come on! I got a little too excited. But you get it, guys. This is going to be the first day of the rest of your life.

[24:41] Right now. I'm Kate. If you like this kind of content, please hit subscribe. Give me a thumbs up. Hit the bell so you know the next time I'm going to be posting a video. I post every Friday.

[24:54] I call it Frugal Friday. And then I always try to post a bonus video sometime earlier in the week. And I hope this has been helpful to you. Please, before you leave, drop a comment below about what part of this budget gets you a little excited.

[25:13] What could happen in the next six months to two years that you would look forward to the most that you will get from budgeting? See you next time. Bye.

[25:26] What's your July budget started today? Do it now guys You got this

⚡ Saved you 0h 25m reading this? Transcribe any YouTube video for free — no signup needed.