Only budget your MINIMUM income

43sThis simple trick ensures you never overspend by using your lowest possible income.

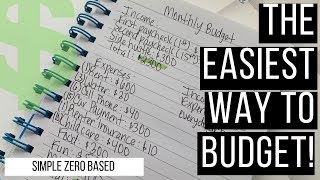

▶ Play ClipThis video provides a step-by-step guide to creating a simple monthly written budget using a notebook. The creator emphasizes the importance of budgeting with take-home pay, listing expenses from most to least important, and giving every dollar a job (zero-based budgeting). The method helped her and her husband pay off $53,000 of debt.

Only list take-home pay after taxes, deductions, and retirement contributions. Budget using the minimum amount you know you'll earn.

Start with fixed expenses (e.g., rent) then variable (e.g., eating out). List from most important (four walls: rent/mortgage, water, electricity, food) to least important.

Always include a miscellaneous category for unexpected items you forgot to budget for.

Income $2,300 minus expenses $1,830 leaves $470. Assign every dollar a job (savings, gifts, extra debt payment) until remaining balance is zero.

Giving every dollar a name prevents mindless spending on unimportant things like eating out or shopping.

Write due dates on a monthly calendar, note paydays, and highlight key items to stay organized.

"The title accurately describes the content: a step-by-step guide to creating a simple written budget."

What income should you use when creating a budget?

Only take-home pay (after taxes, deductions, retirement).

00:30

Should you budget using the average or minimum expected income?

The minimum amount you know you will bring in.

00:47

What are the two main categories of expenses mentioned?

Fixed expenses (don't change) and variable expenses (do change).

01:43

What are the 'four walls' in budgeting?

Rent/mortgage, water, electricity, food.

02:10

What is the zero-based budget principle?

Income minus expenses equals zero (every dollar assigned a job).

04:43

Why should you include a miscellaneous category?

To cover unexpected items you forgot to budget for.

02:53

How much debt did the creator and her husband pay off using this method?

$53,000 of debt.

05:35

Budget with minimum income

Prevents overspending when income varies month to month.

00:47Prioritize the four walls first

Ensures essential needs (shelter, utilities, food) are covered before discretionary spending.

02:10Give every dollar a job

Zero-based budgeting eliminates idle money that often gets wasted.

04:43Paid off $53k debt

Demonstrates the real-world effectiveness of this simple budgeting method.

05:35[00:00] Hello everyone and welcome back to my channel. So today I'm going to be sharing with you guys how to create a simple monthly budget, a written budget to be specific. And I'm using this notebook from Walmart. Obviously there are a bunch of ways that we could budget such as Excel worksheets and budget apps and other electronic methods.

[00:18] But oftentimes it's worth just using a notebook or a regular piece of paper. So the first thing that we want to do is calculate our monthly income and we want to only list our take-home pay.

[00:30] So that's money after taxes, after payroll deductions, after retirement if you have money coming out of your checks for retirement. This is the money that is going to come home to you and the money that will for sure cross your bank account.

[00:47] So you want to budget using the minimum amount that you know you will bring in. obviously sometimes with PTO and just picking up different shifts and working multiple jobs we are able to bring in various amounts but we want to make sure

[01:01] we are budgeting using the absolute minimum that we will bring in so for purposes of this video I'm going to be budgeting for or with $2,300 so we want

[01:13] to total that up so that math is quite easy but if you need a calculator to do your math then obviously go ahead and do that but 1000 plus 1000 plus 300 is $2,300 so that

[01:25] is going to be the total income for the month and this can go for any month this is for no month in particular this is just pretty much how to start out step two is to calculate and list all bills and expenses So I like to start with typically I like to start with fixed expenses first Those are expenses that do

[01:43] not change from month to month and then I like to go to variable expenses which are expenses that do change from month to month. So rent is typically a fixed expense and eating out or personal spending

[01:56] money or gift money is oftentimes categorized as a variable expense. But I will tell you that I feel like the best way to do this is to list the most important expenses first. So a lot of times that

[02:10] is your four walls. So your rent or mortgage, your water, your electricity, your food budget, just start listing your bills and expenses from most important to least important. Because a lot of

[02:22] times if you're down to you know you've got you've gone through all of your bills and all of your more important expenses and you're running a little short on money then a lot of times that means that you may not get to spend fun money for that month or you'll have a little less for fun

[02:38] money or you won't have a lot for eating out so it's important that we're making sure that our four walls are taken care of and we're budgeting for the most important bills and expenses first and foremost. So I always like to leave in a miscellaneous category and this is

[02:53] just for unexpected items. A lot of times we forget to budget for things. I do it all the time. I forgot to budget for my friend's anniversary gift this month and it just happens. So I always like to leave a little bit in miscellaneous and

[03:06] this is just a mock budget Obviously I don have child care or a car payment or some of these other expenses but I just wanted to throw in just some different expenses and not list our expenses

[03:18] So obviously, what we need to do now is total up our expenses. So that is what you see me doing at this very moment. I am adding up the rent, water, cell phone, car payment, renter insurance, child care, food, fun, and miscellaneous.

[03:32] That gives us a total of $1,830. So our next step, of course, is to subtract our expenses from income. So our income is $2,300. Our expenses are $1,830, and that gives us $470.

[03:49] Now, at this point, it's essentially crunch time. So we have to figure out what exactly we're going to do with that $470 or our remaining funds. So this is where a lot of people decide on if they want to go ahead and purchase a gift for somebody.

[04:04] if they want to go ahead and put some towards savings if they want to go ahead and take a small staycation if they want to go ahead and make an additional debt payment so in this video I am

[04:17] actually giving up um the funds just in different categories so I'm not sending all 470 to debt or anything like that and I will show you that momentarily as soon as I slide the page up I

[04:29] I will show you how I am giving up those funds. So I have 200 going towards savings, 30 going towards a gift, and an additional 240 going towards the car payment. At that point, we have spent all of the 470,

[04:43] which is bringing our new remaining balance down to zero I believe that it is absolutely pertinent that we give every single dollar a job an assignment a name and we budget all

[04:55] of our income all the way down to zero and that doesn't mean we take our bank account to zero that just means that we budget for all of our income that is super important because had we not done that then we wouldn't know exactly what

[05:07] to do with the 470 if we just had it just randomly hanging around because nine times out of ten it would go to something that's not important like eating out or shopping or just excess spending um another thing that you can do is write in your due dates for your bills

[05:23] i like to use monthly calendars to write in my paydays in my bills but um a lot of people just kind of mark whenever their bills are due and that works for them so anyway this is pretty much the

[05:35] end of this video i just wanted to show you guys how to compose a simple monthly budget this is a a tried and true every dollar zero base budget and this is the method that my husband and I have used over the last couple of years to pay off $53,000 of debt and to meet some of our other financial

[05:51] goals and I did use a highlighter of course because I'm just a little bit extra but I could definitely get behind this method of budgeting easily. Also one last thing that you can do to really be organized with your finances is to maybe just write in all of the expenses that you have

[06:07] for each month, all of the regular expenses, the irregular expenses, birthdays that are coming up, trips that are coming up, anything that you can write in so that you can prepare yourself for financially. So that is it for this video. I hope that you guys enjoyed it and you learned from it

[06:22] and I will see you in my next one. Bye guys.

⚡ Saved you 0h 06m reading this? Transcribe any YouTube video for free — no signup needed.